Nov 2022

Prices flattening but some homes still sell quickly.

The fed has again raised interest rates and that has cooled the buyer frenzy that we have seen over the last 2 years. However it is felt that interest rates will drop in 2023 and the worst may be over. Despite this environment we recently listed and sold 1542 Melanie Way Livermore Ca 94550 for asking price $1,500,000 in only 12 days. Correct home preparation is critical and again with the presale package we apply at SRG and with professional staging and photography we were successful

and ended with another happy seller.

1542 Melanie Way Livermore Ca 94550 just sold for full price

July 2022

Homebuyer Demand is Slowing

The housing market continues to show signs of slowing. Although Redfin is not the only real estate company in the country, they seem to be reporting the most about the changing housing market versus other national real estate firms. Redfin reported another double-digit decline in homebuyer demand when compared to the same time last year. This is the second time they have reported a decline in the last three weeks.

Redfin's homebuyer demand index was down 12% annually for the week of June 5, compared to a 9% decline for the last week of May and a 12% decline from the week before that. This is the largest index drop since the pandemic's early days.

It is clear that more and more sellers are no longer in control of home prices with bidding wars. Repeatedly, we hear stories of sellers reducing their home prices to increase traffic.

However, let's not assume that the housing boom is over. Despite home prices declining and mortgage rates rising, we are seeing some buyers return to the market. Housing inventory is increasing, offering purchasers more homes to choose from. It has been quite some time since buyers have had this many homes to choose from and not have to enter a bidding war.

Mortgage Rates, Home Prices Expected To Stabilize, Forecast Says

The housing and stock markets have been troubled by the quick rise in mortgage rates and inflation since 2022. Fears of a recession and general economic instability have caused analysts to adjust their year-end estimates to account for these changes.

The housing market is projected to alter in the coming year, but not all changes will be unpleasant. Some respite may be on the way for purchasers who have been dismayed by the shortage of available homes and fierce competition. Furthermore, while mortgage rates and property prices are unlikely to fall, they are predicted to steady and may relieve purchasers who have been trying to keep up with escalating costs and rates.

As demand cools and supply rises, Realtor.com updated its home market projection for 2022 and concluded that calmer waters might be ahead. According to the revised prognosis: Mortgage rates will average 5 percent in 2022, rising to 5.5 percent by the year's conclusion. This compared to an initial projection of a 3.3 percent average increase and a 3.6 percent increase. Moreover, buyer demand is projected to decline over the summer, but most markets will continue to favor sellers.

Fed Hikes Interest Rate Benchmark By 0.75 Percentage Point, The Biggest Increase Since 1994

The Federal Reserve took its most aggressive stance against inflation yet on Wednesday, boosting benchmark interest rates by three-quarters of a percentage point, the most significant increase since 1994.

The Federal Open Market Committee, which sets interest rates, raised its benchmark funds rate to 1.5 percent -1.75 percent, the highest level since just before the Covid epidemic began in March 2020. After the decision, stocks were unstable, but they rose when Fed Chairman Jerome Powell spoke at his post-meeting news conference.

"We want to see progress. Inflation can't go down until it flattens out," Powell said. "If we don't see progress ... that could cause us to react. Soon enough, we will be seeing some progress," Powell said. Based on one widely cited metric, FOMC members projected a significantly steeper path of rate increases to stop inflation from reaching its highest level since December 1981.

According to the midpoint of the goal range of individual members' views, the Fed's benchmark rate will end the year at 3.4 percent. This represents a 1.5 percentage point increase above the March estimate. The committee predicts that the rate will rise to 3.8 percent in 2023, an entire percentage point more than the March forecast.

June 2022

Mortgage Demand Falls To Lowest Level Since December 2018

According to the Mortgage Bankers Association's seasonally adjusted index, mortgage applications for home purchases declined 1% last week compared to the previous week. Despite a slight drop, mortgage rates are still much higher than at the beginning of the year – this, as the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 5.33% from 5.46%, with points dropping to 0.51 from 0.60 (including the origination fee) for loans with a 20% down payment.

Rising interest rates and rapid increases in housing prices are putting a strain on affordability. Because there is still so little supply on the market, prices are continuing to rise, but various levels of purchasers see different pictures. Refinance applications, which are more susceptible to rate changes than purchase applications, declined 5% this week and were 75% lower than last year. Although rates have dropped from their highs in recent weeks, refinance demand has remained flat because many borrowers took advantage of the low rates last year.

Factors That Could Influence Sellers' Behavior

The "rate lock-in effect," as economists define it, occurs when we bind ourselves to the low mortgage rates we received when we bought or refinanced our homes. So, we stay put even though we want to move up, downgrade, or relocate.

Rate lock-in is not without risk (and should not be confused with "locking" an interest rate before closing on a mortgage). It takes properties off the market when demand for housing outstrips supply, driving up prices and encouraging brutal competition. Because they don't have any equity to transfer into down payments, first-time home purchasers are particularly disadvantaged. Is rate lock-in, however, a real thing? How many moves does it obstruct? For more than 40 years, economists have debated the topic.

Quigley and others discovered more evidence of the lock-in effect in the 2000s and 2010s, but experts disagreed on its significance. Rate lock-in is challenging to quantify because consumers relocate or stay for various reasons. And no one pays attention to it until mortgage rates rise dramatically.

House Hunters Take Note: The Blazing-Hot Housing Market Is Finally Cooling Down

A blazing hot housing market is beginning to chill across the United States, giving potential homeowners optimism after months of searching for a new house amid the most challenging conditions in decades.

According to analysts, rising mortgage rates and surging property prices have caused some homebuyers to abandon the market entirely, reducing competitiveness. Because fewer people are competing for the same house, asking prices and the number of properties sold has dropped significantly.

People don't like that today's mortgage rates add hundreds of dollars to monthly payments. This week, the average interest rate on a fixed 30-year mortgage was 5.3 percent. Realtor.com Chief Economist Danielle Hale told CBS News that this is a 13-year high.

Although the dream of homeownership has been pushed out of reach for many middle-class Americans this spring, analysts say the summer may be a better time for those who want to stick it out.

Real estate tracker data released this month indicates that the market is cooling. For instance:

The number of existing homes sold fell 2.4% last month, the third straight month of declines, the National Association of Realtors said.

According to data from the Mortgage Bankers Association, mortgage applications dropped 1% last week and 11% the week before that.

According to Redfin, about 1 in 5 U.S. home sellers lowered their price at some point in May, the highest number of drops since October 2019. Rochester, New York; Detroit, Michigan; and Toledo, Ohio, have seen some of the most significant price drops, according to Realtor.com.

According to U.S. Census data released this week, sales of newly built homes fell 16.6% in April.

The realtors association said Thursday that pending home sales fell almost 4% between March and April.

May 2022

Housing Supply Finally Improving, As High Prices and Rising Rates Weigh on Sales

According to new data from Realtor.com, the supply of properties for sale could expand in the coming weeks. Inventory was down 12% in April compared to the same month last year, the smallest year-over-year drop since 2019. The change in supply is most likely due to a slower sales volume caused by the recent abrupt spike in mortgage rates, which has made already expensive properties considerably more costly.

Some areas of the country already see more homes coming on the market. As well, traffic at open houses has declined. The likelihood of home prices experiencing a significant drop remains low due to the fact there is still considerable demand. However, bidding wars for homes are decreasing in many markets. This could be the beginning of the market adjusting to a more balanced relationship between buyers and sellers.

Inflation Barreled Ahead At 8.3% In April from A Year Ago, Remaining Near 40-year Highs

The Bureau of Labor Statistics said Wednesday that inflation jumped again in April, continuing a trend that has pushed consumers to the edge and put the economy in jeopardy. The consumer price index, a comprehensive measure of prices for goods and services, rose 8.3 percent from a year ago, beating the Dow Jones forecast of 8.1 percent - a modest drop from the peak in March, but it was still near the most significant level since 1982.

Even after removing volatile food and energy costs, the core CPI jumped 6.2 percent, despite predictions of a 6% increase, casting doubt on optimism that inflation had peaked in March. The month-over-month increases were also more significant than expected, with headline CPI up 0.3 percent versus a forecast of 0.2 percent and core CPI rising 0.6 percent versus a forecast of 0.4 percent.

Officials at the Federal Reserve have responded to the crisis with two interest rate hikes this year and promise more until inflation falls below the central bank's target of 2%. Markets were hoping that March's 8.5 percent CPI reading would be the highest since the pandemic began. However, the April report showed that "this is another upward inflation surprise and suggests that the deceleration is going to be painstakingly slow," said Seema Shah, chief strategist at Principal Global Investors.

MBA Weekly Applications Survey May 11, 2022: Winning Streak at 2

Mortgage applications grew for the second week in a row, despite interest rates reaching a 13-year high, according to the Mortgage Bankers Association's Weekly Mortgage Applications Survey for the week ending May 6. The Market Composite Index increased 2.0 percent over the previous week on a seasonally adjusted basis. On the other hand, the unadjusted Refinance Index dropped by 2 percent from the prior week. The refinance share of overall mortgage applications fell to 32.4 percent from 33.9 percent the previous week. The seasonally adjusted Purchase Index increased by 5 percent from one week ago. The FHA's percentage of overall applications fell to 10.5 percent this week, and the rate of total applications submitted by veterans grew to 10.5 percent, up from 10.3 percent the week before. The USDA's proportion of overall applications rose from 0.4 percent early to 0.5 percent.

"Despite a slow start to this year's spring homebuying season, prospective buyers are showing some resiliency to higher rates. Purchase activity has now increased for two straight weeks," said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. Kan stated that more customers continue to utilize adjustable-rate mortgages to offset rising rates.

Moreover, MBA reports that the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) jumped to 5.53 percent from 5.36 percent, with points jumping to 0.73 from 0.63 for 80 percent loan-to-value ratio loans. The effective rate has risen since the previous week.

MBA Weekly Applications Survey April 20, 2022: Rising Mortgage Rates Push Down Applications

Mortgage application activity fell last week due to the highest mortgage rates in more than a decade, according to the Mortgage Bankers Association'sAssociation's Weekly Mortgage Applications Survey for the week ending April 15TH.

The Market Composite Index fell 5.0 percent from the previous week on a seasonally adjusted basis. The refinance share of mortgage activity decreased to 35.7 percent of total applications from 37.1 percent as Refinance Index dropped by 8 percent. Moreover, the seasonally adjusted Purchase Index also fell by 3 percent.

"Ongoing concerns about rapid inflation and tighter U.S. monetary policy continued to push Treasury yields higher, driving mortgage rates to their highest level in over a decade," said Joel Kan, MBA Associate Vice President of Economic and Industry Forecasting. "The 30-year rate has increased 70 basis points over the past month and is two full percentage points higher than a year ago. The recent surge in mortgage rates has shut most borrowers out of rate/term refinances."

Homeowners Don't Want To Sell, Prices Will Likely Remain High

The housing market in the United States has been troubled by a record low inventory of homes for sale for months, resulting in heightened competition and record-high prices. As a result, home prices have risen 19.2 percent in the last year, putting many potential buyers out of the market. With prices beginning to slow, the housing market appears to be entering a cooling period. However, the number of homes for sale continues to be insufficient. Moreover, two new housing reports imply that the same policy now cooling the housing market may prevent inventories from rebounding.

Over the last five years, two variables have converged to push prices this high. First, the early-pandemic low mortgage rates stimulated demand for housing, while the supply of new homes remained at historic lows, resulting in intense competition and higher prices. However, that relationship is now crumbling, and the equation is shifting.

Low mortgage rates used to be the safety net that allowed people to buy houses even when they couldn't afford them. That cushion is now gone, as most current homeowners enjoy fixed rates that are substantially lower than what they would face if they were to sell. More listings and homes on the market would significantly reduce competition, provide buyers more bargaining power, and keep prices in check. New house construction starts in the United States are steadily increasing, which is a positive indication. Still, supply will remain tight until current homeowners return to the market, which means prices will likely remain high.

Builder Confidence Remains Resilient Despite Rising Rates

Although mortgage rates are at their highest in over three years, the housing industry has yet to show symptoms of trouble. The NAHB/Wells Fargo Housing Market Index (HMI) released in April is the most recent data to support that premise.

While the headline HMI number is identical to builder confidence, it is still in comparatively high territory, down marginally from the previous month's reading. The HMI and the "buyer traffic" indicator were more significant than before the covid-fueled real estate boom.

While the 6-month forecast isn't as optimistic as the other HMI components, it has improved from last month. The industry faces significant headwinds due to the high rate of home price rise mixed with one of the most considerable mortgage rate spikes in history. As a result of these challenges, the HMI has fallen from recent highs. However, the fact that those levels are still high by historical standards reflects resilience. But despite this, NAHB Chief Economist Robert Dietz was not optimistic. He stated that "the housing market faces an inflection point as an unexpectedly quick rise in interest rates, rising home prices, and escalating material costs have significantly decreased housing affordability conditions, particularly in the crucial entry-level market."

April 2022

Sellers market still

September 2021

Median prices continue to rise…

July 2021

Check this out, prices continue to rise….

LIVERMORE,CA

Wed June 2 2021

We had a couple of ‘slower weeks for sales but have bounced back with a stronger weekend last.

Inventory now stands at around 85 homes for sale in Livermore, still very low so the sellers market is still strong, prices have seemed to plateaud, but sales are brisk, most homes selling within 14 days on the market. Open houses are now allowed but many agents and sellers dont see the need, this hangover from the 1970s and 80s may be a thing of the past. Online presence is what sells property today.

Livermore, CA

Wed April 7 2021

Without a doubt we are in the strongest sellers market I have ever seen. Only 55 homes for sale in Livermore, very tight supply with above average buyer activity has caused prices to skyrocket, great for sellers, tough for buyers, but can it last?

Livermore, CA

Tue Aug 11 2020

This week the median list price for Livermore, CA is $924,475 with the market action index hovering around 85. This is an increase over last month's market action index of 72. Inventory has held steady at or around 58 homes for sale (not a lot).

Market Action Index

This answers “How’s the Market?” by comparing rate of sales versus inventory.

ITS a Strong Seller's Market!

Home sales continue to outstrip supply and the Market Action Index has been moving higher for several weeks. This is a Seller’s market so watch for upward pricing pressure in the near future if the trend continues.

Real-Time Market Profile

Median List Price is $924,475

$482 Days on Market

65 have a Price Decrease

21% have a Price Increase 2% were Relisted

58 Median Rent is $3,000

Most Expensive house for sale $68,000,000

Least Expensive$130,000 Market Action Index is

85 meaning a Strong Seller's Market!

May 29 2020

COVID -19 Is it the end for home sales in Livermore?

Answer a resounding NO!

I am busier than ever! Buyers are still buying, inventory is relatively low and although as agents we no longer are currently able to have Broker tours or open houses who needs them? Houses are selling uising modern 3D walkthrough tours like this one…

Inventory still very low.

Usually once the weather warms up more property becomes available and likely it will soon, however as of now the existing supply of homes for sale remains near record lows. This has resulted in mul;ti[ple offers for most properties if they look good and are priced correcly, and sales prices higher that asking in most cases.

Lower than average inventory and high buyer demand = opportunity

FEBRUARY 2017, Inventory is sinking like a rock! NOW is the time to sell, don't wait till the spring like...

your (friend/collegue at the office/ Zillow article you happened to read or aunt Mildred) said, do it now and get more offers and a higher price because you have less competition! See for yourself!

Why do sellers still wait for spring? Go figure!

December 2017 Livermore statistics;

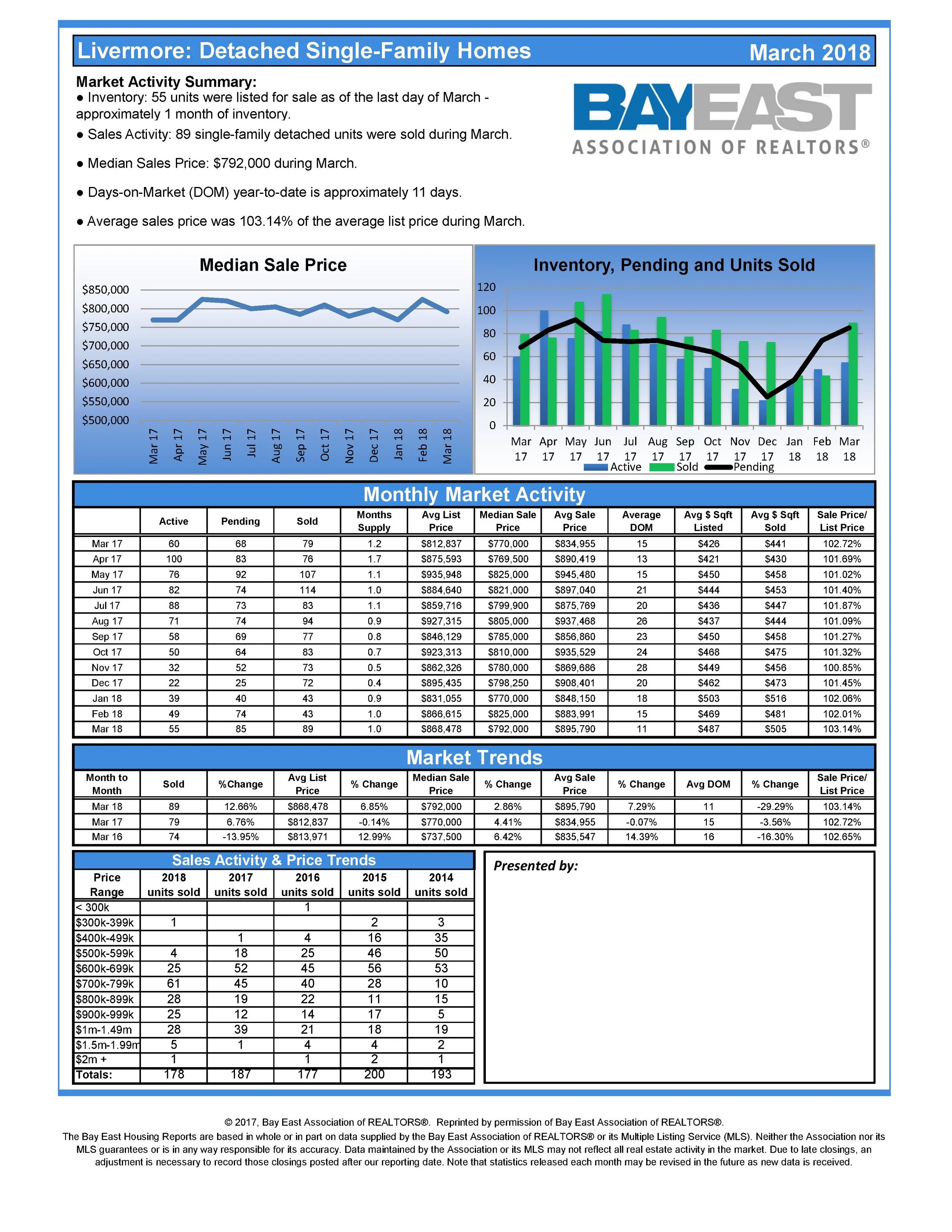

March 2018 single family home stats showing a lively market, normal for the time of year

Mortgage Demand Falls To Lowest Level Since December 2018

According to the Mortgage Bankers Association's seasonally adjusted index, mortgage applications for home purchases declined 1% last week compared to the previous week. Despite a slight drop, mortgage rates are still much higher than at the beginning of the year – this, as the average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 5.33% from 5.46%, with points dropping to 0.51 from 0.60 (including the origination fee) for loans with a 20% down payment.

Rising interest rates and rapid increases in housing prices are putting a strain on affordability. Because there is still so little supply on the market, prices are continuing to rise, but various levels of purchasers see different pictures. Refinance applications, which are more susceptible to rate changes than purchase applications, declined 5% this week and were 75% lower than last year. Although rates have dropped from their highs in recent weeks, refinance demand has remained flat because many borrowers took advantage of the low rates last year.

Factors That Could Influence Sellers' Behavior

The "rate lock-in effect," as economists define it, occurs when we bind ourselves to the low mortgage rates we received when we bought or refinanced our homes. So, we stay put even though we want to move up, downgrade, or relocate.

Rate lock-in is not without risk (and should not be confused with "locking" an interest rate before closing on a mortgage). It takes properties off the market when demand for housing outstrips supply, driving up prices and encouraging brutal competition. Because they don't have any equity to transfer into down payments, first-time home purchasers are particularly disadvantaged. Is rate lock-in, however, a real thing? How many moves does it obstruct? For more than 40 years, economists have debated the topic.

Quigley and others discovered more evidence of the lock-in effect in the 2000s and 2010s, but experts disagreed on its significance. Rate lock-in is challenging to quantify because consumers relocate or stay for various reasons. And no one pays attention to it until mortgage rates rise dramatically.

House Hunters Take Note: The Blazing-Hot Housing Market Is Finally Cooling Down

A blazing hot housing market is beginning to chill across the United States, giving potential homeowners optimism after months of searching for a new house amid the most challenging conditions in decades.

According to analysts, rising mortgage rates and surging property prices have caused some homebuyers to abandon the market entirely, reducing competitiveness. Because fewer people are competing for the same house, asking prices and the number of properties sold has dropped significantly.

People don't like that today's mortgage rates add hundreds of dollars to monthly payments. This week, the average interest rate on a fixed 30-year mortgage was 5.3 percent. Realtor.com Chief Economist Danielle Hale told CBS News that this is a 13-year high.

Although the dream of homeownership has been pushed out of reach for many middle-class Americans this spring, analysts say the summer may be a better time for those who want to stick it out.

Real estate tracker data released this month indicates that the market is cooling. For instance:

The number of existing homes sold fell 2.4% last month, the third straight month of declines, the National Association of Realtors said.

According to data from the Mortgage Bankers Association, mortgage applications dropped 1% last week and 11% the week before that.

According to Redfin, about 1 in 5 U.S. home sellers lowered their price at some point in May, the highest number of drops since October 2019. Rochester, New York; Detroit, Michigan; and Toledo, Ohio, have seen some of the most significant price drops, according to Realtor.com.

According to U.S. Census data released this week, sales of newly built homes fell 16.6% in April.

The realtors association said Thursday that pending home sales fell almost 4% between March and April.